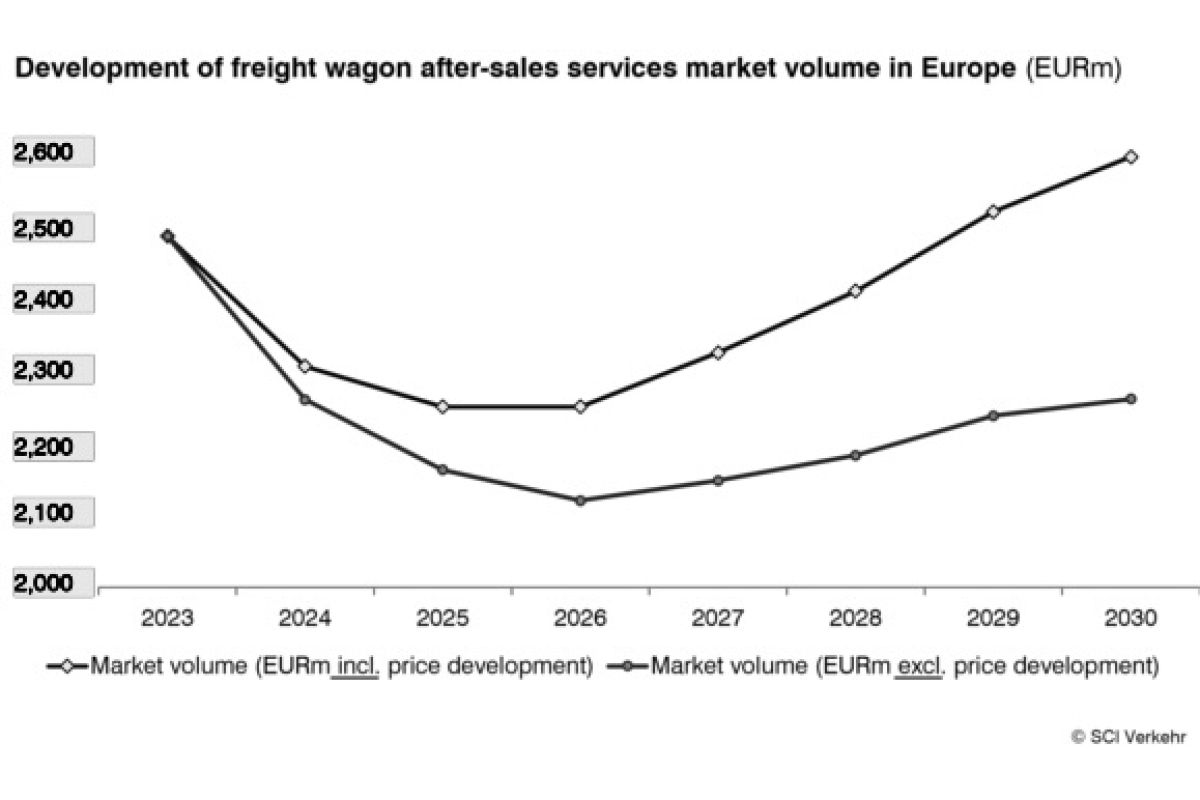

Demand for maintenance and repair services in rail freight is falling as Europe’s freight-transport sector continues to struggle. According to SCI Verkehr’s new study “Rolling Stock Maintenance – Global Market Trends”, the European freight-wagon maintenance market—currently worth EUR 2.3 billion—is expected to grow only marginally by 2030.

Workshops serving freight locomotives and wagons are being hit by both the economic slowdown and deeper structural issues. Traditional bulk transport such as steel and coal continues to decline, while automotive and chemical flows are also weakening. Financial difficulties at former state freight operators — SNCF, DB Cargo and PKP Cargo — are contributing to the shrinkage of single-wagonload networks, reducing the volume of rolling stock entering maintenance cycles.

Globally, the market for rolling-stock maintenance stands at EUR 87 billion and is projected to exceed EUR 100 billion by 2030, representing average annual growth of around 3.5%. Maintenance remains a predominantly local business, but supply chains for components are under pressure, with prices rising and delivery times lengthening due to US customs policy, particularly for foreign manufacturers.

The study highlights stronger performance in the passenger-rail MRO segment, where long-distance services and high-speed fleets require more full-service and performance-based maintenance. Demand related to diesel multiple units is weakening as rail networks electrify and operators shift interest toward alternative traction technologies.

Urban transport is identified as the fastest-growing MRO segment worldwide. Metro fleets purchased in the early 2000s are now undergoing major mid-life upgrades, particularly for energy-efficiency improvements. The after-sales market for light rail vehicles (LRVs) also shows steady growth linked to network extensions and accessibility upgrades, even though fleet sizes expand only moderately.

Similar to Europe, the global maintenance market for freight rolling stock is showing structurally limited growth, with expectations turning negative in some regions. The study concludes that the freight sector’s weakness is increasingly reflected in workshop utilisation, investment planning and long-term MRO capacity across multiple markets.