Europe has become the world’s largest market for control, command and signalling (CCS) technology, overtaking China as pressure grows to modernise ageing rail infrastructure and expand network capacity.

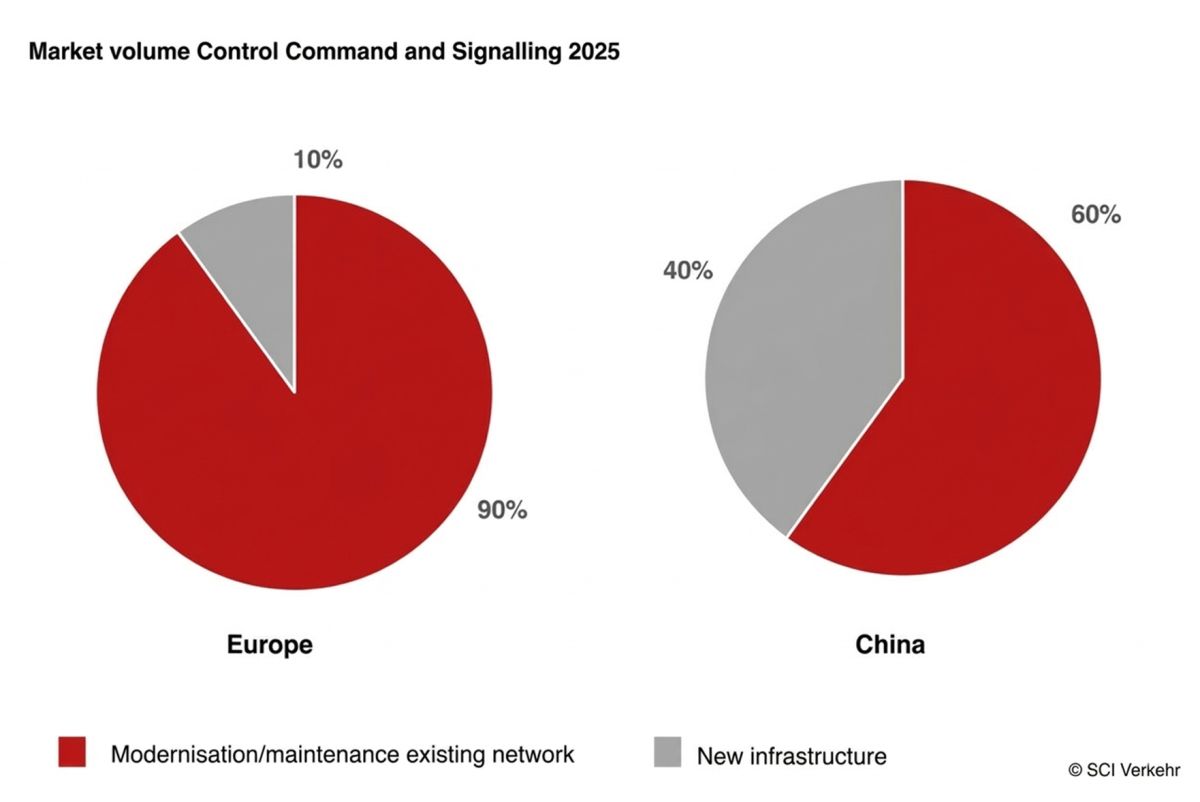

According to a new market study by SCI Verkehr, Europe now accounts for almost half of the global CCS market, which is estimated at around €20 billion. The main driver is not large-scale new construction, but the renewal and digital upgrading of existing networks. On the chart included in the study, around 90% of the European CCS market in 2025 is linked to modernisation and maintenance of the current network, while only 10% is associated with new infrastructure.

SCI Verkehr argues that outdated signalling systems are becoming increasingly unsustainable from both an operational and financial perspective. In Europe’s dense and complex rail networks, newer CCS systems are seen as one of the few realistic ways to increase capacity, lower long-term costs and improve reliability without relying solely on new lines. As a result, the consultancy expects Europe to record the fastest CCS market growth globally by 2030.

At the same time, the report underlines that Europe still lags behind Asia in overall signalling standardisation and deployment. Interoperability remains a structural challenge, with national approaches continuing to slow the harmonisation of train control systems. The rollout of ETCS has been postponed repeatedly in several countries, meaning that the gap between political ambition and implementation remains visible across the continent.

Over the next decade, the European market is expected to be shaped above all by ETCS, digital interlockings and progress in FRMCS, the future railway mobile communication system intended to replace GSM-R. Together, these technologies are increasingly viewed as the backbone of rail digitalisation, linking signalling, train protection, communication and operational control more closely than before.

China remains the dominant force within Asia, accounting for more than 65% of the regional CCS market. There, growth is still being driven by high-speed and metro expansion, although at a slower pace than in the previous decade. At the same time, China is pushing ahead with digital and automated rail operation, including large-scale investment in modern train control and 5G-based railway communications.

Globally, train control systems now represent the largest product segment in the CCS market, accounting for around 40% of total volume. SCI Verkehr says these systems are driving a broader technological shift, enabling more efficient use of constrained infrastructure, automated operations, better energy performance and higher passenger comfort. New generations of ETCS and CBTC are also stimulating demand in adjacent segments such as digital interlockings and operational telematics.

The study also points to strong momentum in urban rail. Metro and commuter rail operators are investing heavily in CCS as cities seek more efficient and lower-emission transport systems. High-speed rail projects in Asia – especially in China – and in Europe are adding further demand for advanced signalling and train control systems.

Overall, the report suggests that the CCS market is entering a new phase in which modernisation is becoming more important than pure expansion, particularly in Europe. For the rail industry, that means signalling is no longer only a technical subsystem: it is increasingly central to capacity strategy, automation, cost control and the wider digital transformation of the railway.